In the world of investments, real estate has long been touted as a reliable hedge against inflation. As prices rise across the economy, property values historically climb too, preserving and often growing wealth in real terms. Yet, as we approach the end of 2025, the U.S. housing market tells a different story. Existing home sales are hovering near 25-year lows, with transactions barely scraping 4 million annually—a far cry from the 6 million-plus peaks of the early 2020s. Meanwhile, inflation ticks along at around 3%, and alternative assets like stocks and gold are booming. So, why aren't more homeowners cashing in, and why are buyers staying on the sidelines? This paradox isn't just a market quirk; it's a confluence of high mortgage rates, affordability barriers, and shifting demographics that's "freezing" the market in place. In this deep dive, we'll explore the roots of this stagnation, backed by the latest data, and what it means for the future.

Real Estate as an Inflation Hedge: The Traditional Wisdom

For decades, real estate has been a go-to strategy for beating inflation. Unlike cash or bonds, which can erode in value as prices rise, properties tend to appreciate alongside or ahead of inflation rates. Historically, during high-inflation periods like the 1970s, home values surged, providing owners with built-in protection. Even in 2025, with inflation moderating to about 3%, experts still argue that real estate outperforms gold in liquidity-constrained environments, as rental income and property appreciation can outpace rising costs.

But here's the catch: this hedge assumes a fluid market where buyers and sellers can transact easily. In today's reality, that's not happening. Home price gains are lagging behind inflation for the first time in years, meaning homeowners are effectively losing real wealth if they hold onto properties without selling. In inflation-adjusted terms, equity erosion is occurring as maintenance costs, taxes, and other expenses climb faster than values in many regions. This challenges the narrative that real estate is always a safe bet—especially when sales volumes are so depressed that liquidity dries up.

A Snapshot of the Sluggish Market: Sales at Historic Lows

Let's look at the numbers. As of September 2025, existing home sales rose modestly by 1.5% month-over-month to an annualized rate of 4.06 million—the highest in seven months, but still near 30-year lows. Zillow's forecast pegs full-year sales at around 4.07 million, a mere 0.3% uptick from 2024. Inventory is up 14% year-over-year, with over 1 million homes listed nationwide, yet median prices have dipped slightly to $400,000 as gains slow.

This stagnation contrasts sharply with the post-pandemic boom. From 2020 to 2022, sales surged as low rates fueled demand. Now, with rates above 6%, the market is in a "deep freeze." Buyers face affordability hurdles, while sellers hesitate, creating a vicious cycle. Even as the Federal Reserve cuts rates, the thaw is slow—monthly principal and interest payments are up 2.9% year-over-year.

To visualize this trend, consider the decline in pending home sales contracts over recent years:

Why the housing market is actually much healthier in 2025

This chart highlights how pending contracts peaked in 2021 and have trended downward, underscoring the market's reluctance to move.

The Mortgage Rate Lock-In Effect: Golden Handcuffs for Homeowners

One of the primary culprits is the "lock-in effect." Over half of U.S. homeowners hold mortgages with rates below 4%, locked in during the low-rate era of 2020-2021. Selling now means facing rates around 6.25%-6.5%, which could double monthly payments on a new home. A Bankrate survey reveals 54% of homeowners wouldn't sell at any rate in 2025, up from previous years.

The Federal Housing Finance Agency estimates this has prevented 1.72 million sales from 2022-2024 alone. It's not just about payments; high equity (from past appreciation) makes owners comfortable staying put, even as inflation nibbles at real gains. As one analyst notes, even a 0% rate wouldn't make homes affordable in some markets due to price levels.

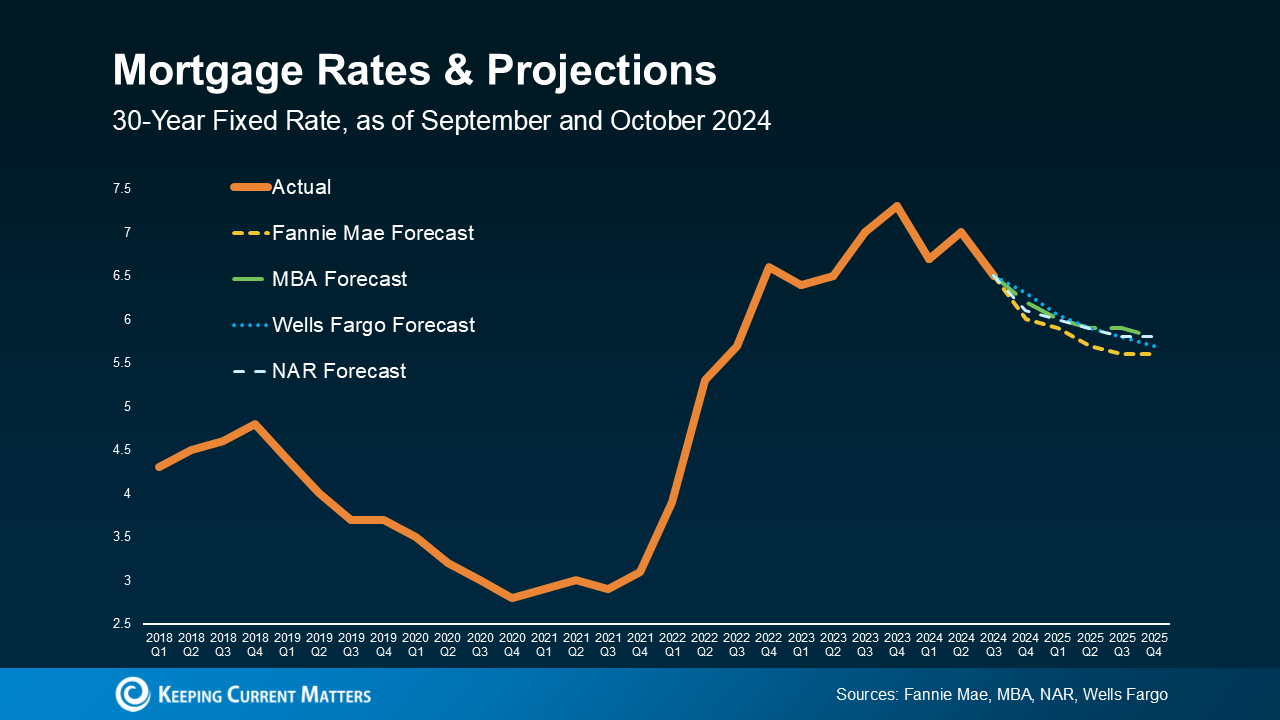

Projections show rates easing further, but not dramatically. Forecasts from Fannie Mae, MBA, NAR, and Wells Fargo predict 30-year fixed rates dipping to 5.5%-6% by Q4 2025.

What To Expect from Mortgage Rates and Home Prices in 2025 ...

Yet, this gradual decline may not unlock enough supply to revive sales volumes significantly.

The Affordability Crunch: Prices Outpacing Wages

Affordability remains a massive barrier. Home prices have risen faster than wages for years, requiring buyers to earn 70% more income for a median home than six years ago. In real terms, prices are weakening—gains are below the 3% inflation rate in many areas, leading to effective declines. The FHFA House Price Index rose just 0.4% in August 2025, signaling stabilization rather than growth.

This crunch sidelines first-time buyers, with more purchases by those over 70 than under 35. Cash buys are up—one in three homes sold in early 2025 were all-cash—favoring investors over average families. In high-cost areas, even declining rates don't help; a Zillow analyst quips that affordability is so strained, rates would need to plummet unrealistically.

Here's a look at year-over-year changes in median sale prices, showing the volatility and recent slowdown:

The Hottest Real Estate Markets [2025 Edition]

Inventory Shifts and Regional Disparities

Inventory is rising—up 14% nationally—but it's uneven. In Florida, prices are declining due to oversupply, while San Francisco remains hot with tight stock. Homes linger on the market longer, with price reductions common in California. This "buyer's market" in some regions contrasts with the overall freeze, as economic uncertainty (like job market fears) keeps demand low.

Demographics play a role too: Aging populations in the Northeast are holding onto homes, while suburban shifts from remote work add complexity.

Broader Economic and Policy Influences

Beyond rates and prices, federal policies have exacerbated the lock-in. Low-rate mortgages from the pandemic era, backed by government programs, have inadvertently locked owners in. Inflation's impact on appraisals and upkeep costs adds pressure, especially if rates stay elevated. Turbulent inflation can strain tenants, leading to defaults and disrupting rental income—a key hedge component.

Post-election policies could shift things, but for now, the market's "frozen" state is expected to persist into 2026, with flat sales and potential builder bankruptcies.

Implications for Buyers, Sellers, and Investors

For buyers, this could mean opportunities: More inventory and softening prices in select markets offer negotiation power. Sellers might need to get creative with concessions or wait for rates to drop further. Investors, meanwhile, see value in rentals or flips, but liquidity risks loom.

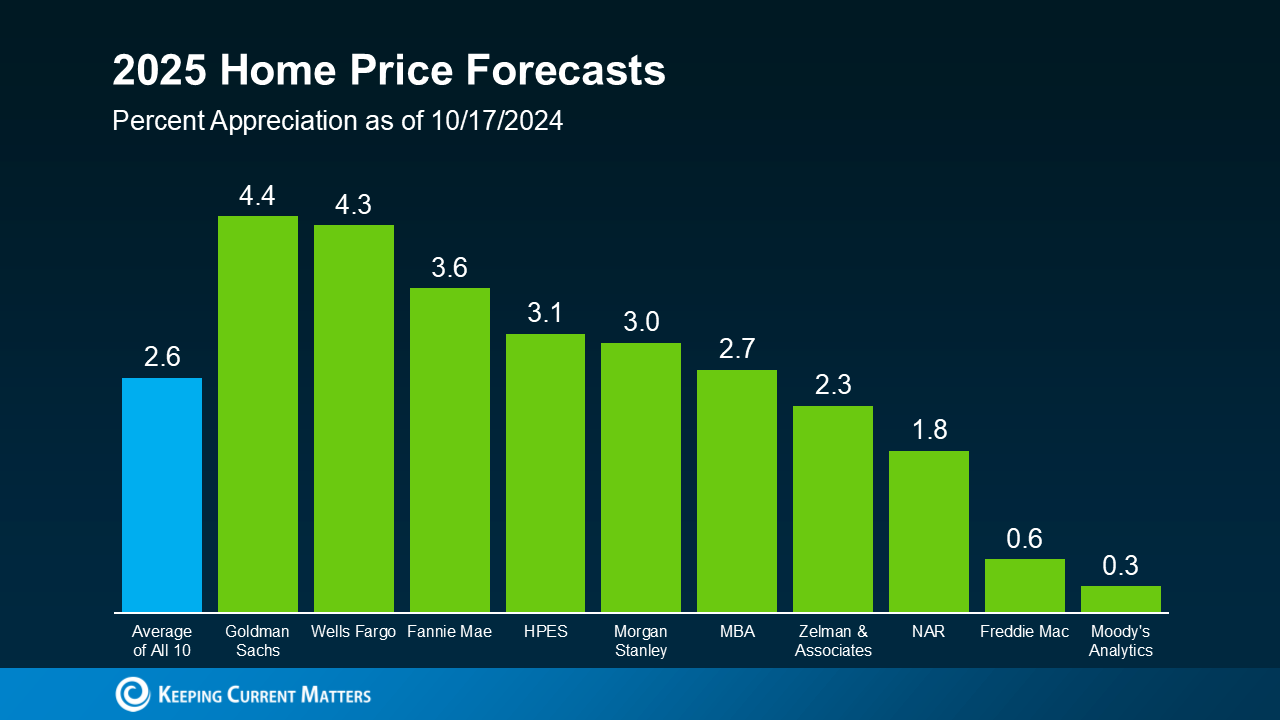

Looking ahead, 2025 home price forecasts average 2.6% appreciation, with some predicting as low as 0.3%.

What To Expect from Mortgage Rates and Home Prices in 2025 ...

If rates fall to 5.5%, sales could rebound to 4.5 million in 2026.

Conclusion: Thawing the Freeze – What Lies Ahead?

The 2025 housing market's lag isn't a rejection of real estate as an inflation hedge—it's a symptom of transitional pains. The lock-in effect, affordability woes, and economic headwinds have created a standoff, but as rates ease and inventory builds, a gradual thaw seems likely. For now, patience is key. Whether you're buying, selling, or investing, staying informed on these dynamics will help navigate this frozen landscape. As always, consult professionals for personalized advice, and keep an eye on upcoming data releases like NAR's October sales report on November 19. The market may be stuck, but history shows it won't stay that way forever.

:strip_icc()/adu-accessory-dwelling-unit-guide-ad2e55fa1d8c47baac5d5baa2f29cd3b.jpg)

![The Hottest Real Estate Markets [2025 Edition]](https://constructioncoverage.com/wp-content/uploads/2025/02/Chart1_Home-Sale-Price-Changes-Over-Time.png)