In the ever-evolving landscape of the U.S. housing market, the idea of a 50-year mortgage has recently gained traction, especially following proposals from the Trump administration aimed at tackling soaring home prices. As of November 2025, with average home prices hovering around $415,200 and interest rates at about 6.17%, many potential buyers are struggling to enter the market. A 50-year mortgage extends the traditional 30-year term by two decades, amortizing the loan over a longer period to reduce monthly payments. But is this extended timeline a smart financial move or a recipe for prolonged debt? In this article, we'll break down the pros and cons, backed by expert insights and real-world examples, to help you decide if it's right for you.

A 50-year mortgage works much like its shorter counterparts: It's a fixed-rate loan where principal and interest are spread out over 50 years instead of 30. This results in lower monthly principal and interest payments, making it appealing in a high-cost environment. However, these loans aren't widely available yet due to regulatory limits—government-backed entities like Fannie Mae and Freddie Mac currently can't insure mortgages longer than 30 years, which would require congressional changes to expand. Proponents argue it could be a "game changer" for affordability, while critics warn of hidden pitfalls.

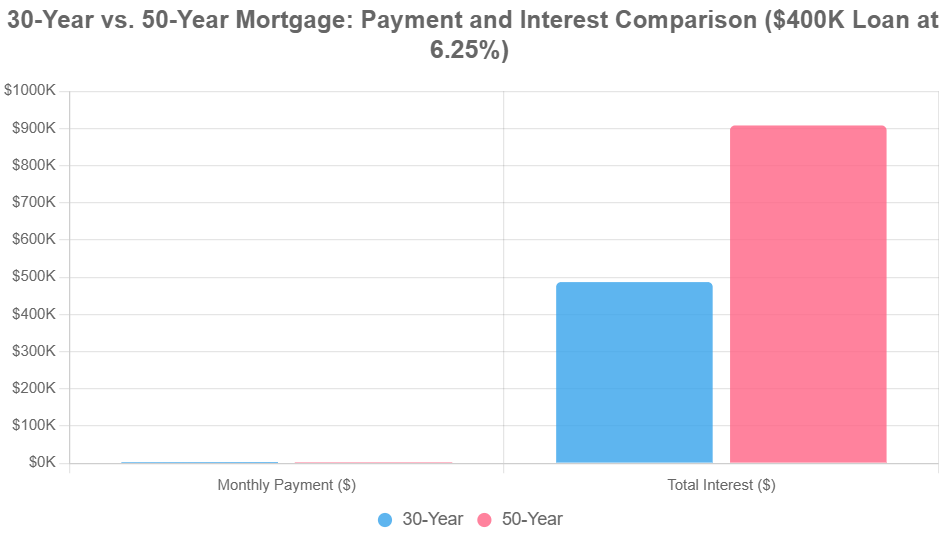

To illustrate, let's look at a comparison based on a $400,000 loan at a 6.5% interest rate (a common benchmark in recent analyses):

| Loan Term | Monthly Payment (Principal + Interest) | Total Payments | Total Interest Paid |

|---|---|---|---|

| 30 Years | ~$2,528 | $910,178 | $510,178 |

| 50 Years | ~$2,255 | $1,352,921 | $952,921 |

Another example for an average-priced home ($415,200 with 10% down, loan of ~$373,680 at 6.17%): A 30-year term yields a monthly payment of $2,288, while 50 years drops it to $2,022—but adds roughly $389,000 in extra interest over the life of the loan.

The Pros of a 50-Year Mortgage

While not a silver bullet, a 50-year mortgage offers several advantages, particularly for younger buyers or those in expensive markets.

- Lower Monthly Payments: The standout benefit is reduced monthly costs, which can free up cash for other priorities like saving for retirement, investing, or even buying additional properties. For instance, on a $400,000 loan, payments drop from about $2,528 to $2,255—a savings of over $270 per month. This can make homeownership accessible for those who might otherwise be priced out.

- Easier Loan Qualification and More Buying Power: Lower payments improve your debt-to-income ratio, helping you qualify for a larger loan or a pricier home. It's a "foot-in-the-door" strategy: Get into the market now and refinance to a shorter term later when rates drop or your income rises.

- Flexibility for Investments: With extra monthly cash, you could invest in stocks, retirement accounts, or even rental properties, potentially outpacing the interest costs if your returns are strong.

- Potential Economic Boost: By bringing more buyers into the market, it could stimulate housing development and economic growth, as increased demand encourages builders to ramp up supply.

Experts like Bill Pulte from the Federal Housing Finance Agency have called it a potential "complete game changer" for first-time buyers facing high costs.

The Cons of a 50-Year Mortgage

Despite the appeal of lower payments, the drawbacks are significant and could impact your long-term financial health.

- Sky-High Total Interest Costs: Extending the term means paying interest for longer, often resulting in nearly double the interest compared to a 30-year loan. In the $400,000 example, you'd pay an extra $442,743 in interest over 50 years. Critics note this could "double the dollar amount of interest paid" on a median-priced home.

- Slower Equity Build-Up: With more of your payments going toward interest early on, it takes far longer to build home equity. For example, it might take 30 years to accumulate $100,000 in equity on a 50-year mortgage, versus just 12-13 years on a 30-year one (excluding appreciation). This delays your ability to tap into home equity for loans or sales.

- Risk of Higher Home Prices and Market Inflation: By boosting demand without addressing supply shortages (estimated at 4.7 million homes), these loans could drive up prices further, making housing less affordable overall. As seen with low rates in 2021, this creates a vicious cycle.

- Longevity and Inheritance Concerns: The average first-time buyer is 40 years old, with a life expectancy of 79—leaving an 11-year gap where debt might pass to heirs.

- Higher Interest Rates and Availability Issues: Lenders view longer terms as riskier, potentially charging higher rates (e.g., 6.75% vs. 6.25%). Plus, precedents in auto and student loans show extended terms lead to higher delinquencies and inflated prices.

Realtor.com's Joel Berner warns that such loans primarily benefit lenders by prolonging high-interest periods, and they won't fix underlying supply issues.

Is a 50-Year Mortgage Right for You?

Ultimately, a 50-year mortgage could suit young buyers in high-cost areas However, for most, the cons—like massive interest accrual and slow equity growth—outweigh the pros, especially if you can afford a 30-year term or explore alternatives like 40-year mortgages (which offer similar benefits with less extreme drawbacks). Remember, you are only saving a few hundred dollars with a 50-year loan vs a 30-year.

Experts emphasize that true affordability comes from increasing housing supply through regulatory reforms, not just extending debt timelines. If you're considering this option, consult a financial advisor to run personalized numbers. What are your thoughts—would you opt for a 50-year mortgage? Share in the comments!

If I can be of any assistance to you or anyone your know, please know I am NEVER too busy for your referrals. I am here when you need me!

Contact me anytime!

Sean Tavalozzi ~ Maryland Realtor

The Old Father Group

Compass

Cell: 203-233-8445

Email: Sean.Tavalozzi@theoldfathergroup.com

No comments:

Post a Comment